We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

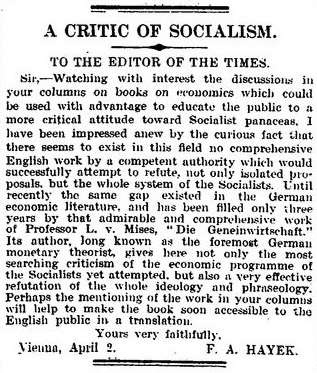

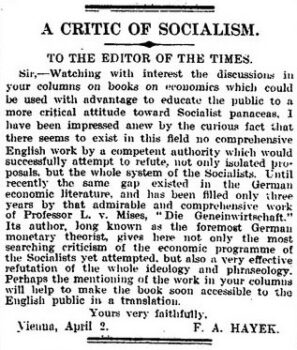

Ernest Benn was the uncle of Tony Benn and great-uncle of Hilary Benn. Luckily for us he was the black sheep of the family and pursued a career in business before becoming one of the “great and the good”. And then he decided he didn’t want to be great or good any more, founding the Society for Individual Freedom. As I understand it the Libertarian Alliance – who most here will be familiar with – emerged from that association.

A hundred years ago Benn was compiling a list of good economics books which – seemingly unbelievably – The Times published. It includes – as you might expect – Smith, Bastiat and Mill and – as you might not expect – Spencer and Smiles. It also includes Henry Ford – presumably before he started blaming the Jews for everything. But there is one book that’s missing. Luckily a young Austrian is on the case.

The Times, Tuesday, 14 April 1925 [I hope this is legible. It’s a bit blurred on my computer but the original is fine. The list is totally blurred if I try to include it inline with the post. All very odd.]

Elliot Keck (who he?) had this recent excellently sharp item over at CapX:

It can be infuriating making the case for free markets. Too much time has to be spent batting away obviously terrible, tried-and-failed ideas. Proposals for a wealth tax are just the latest iteration requiring many a wall to be bashed with many a head. Just in the last few days, a group called ‘Patriotic Millionaires’ has urged Rachel Reeves to consider a ‘simple way’ to grow the economy with a tax of 2% on wealth over £10 million per year. A recent piece in the New Statesman concluded that a wealth tax wouldn’t be straightforward, but it could work. The new director of the Institute for Fiscal Studies has also called for a one-off wealth tax.

This is mad. As a TaxPayers’ Alliance study of wealth taxes has demonstrated, they’ve failed everywhere they’ve been tried. When Labour considered one in the 1970s, they concluded it would be unworkable, despite capital being far less mobile then than it is today.

We are already seeing the wealthy flee at a shocking rate (just look at the Adam Smith Institute’s millionaire tracker), forced abroad by changes to non-dom rules, punitive marginal tax rates, shoddy public services, increasing crime and the imposition of VAT on private schools, to name just a few incentives. When this is pointed out to proponents of wealth taxes, as I recently found on LBC, the response is not to dispute the problem but to bemoan the fact that every time the rich are asked to pay their ‘fair share’, they throw their toys out the pram and flee.

Yet now those who have the temerity to be affluent are being told to cough up to clean up the almighty mess made by our political class. It’s yet another reason for the wealthy to line up for the last chopper out of Saigon. Rather than criticising those who leave, we should increasingly be thanking those who choose to stay.

“America doesn’t make anything anymore” is a powerful talking point, but it’s false. We make plenty, including some of the most complex, high-valued goods in the world, from aircraft to pharmaceuticals to advanced electronics. Our workers don’t make many T-shirts or toasters; other countries can do it more cheaply. And the more successfully we produce and export advanced machinery, the more foreign goods we can afford to import. America’s industrial base is not collapsing. It’s evolving—becoming more productive, more specialized, and more capital-intensive. Protectionism won’t bring back the past or revive old jobs. It will just make the future more expensive and shift workers into lower-paying jobs.

– Veronique de Rugy, Reason magazine.

Lest any Trump admirers get all upset about my posting this quotation it is worth pointing out that there is plenty of protectionist guff on my side of the Atlantic as well. The EU has its Customs Union – the aspects of the bloc that I like the least – and it is described in typically bureaucratic fashion, here. This article in the Financial Times contains the claim that the EU is not as comprehensive in its “protective shields” as the US, Canada and Australia. That said, free trade in general terms is in global retreat, unfortunately, and not simply under the Trump administration – previous US governments were hardly much better, although that is not setting the bar very high.

I have jousted a bit in the comments on previous threads with those claiming that tariffs are necessary, for various (and to my mind, fallacious and often self-contradictory reasons): to “protect jobs”; national security and diversification of supply; as a club to hit supposedly foolish and oppressive other countries; to raise taxes and shift away from income taxes, or that comparative advantage on the David Ricardo model does not work if you allow cross-border capital flows. All the arguments are, in my view, flawed and in some cases, just plain wrong. (Here is a good summary of the arguments contra protectionism.)

As it is used a lot these days, here’s a good take-down, from the Hoover Institution, of the “national security” argument for tariffs. I can also recommend a new book, Free Trade In The 21s Century, a collection of essays by folk from the political, business and economics world. It is a big read, but good to immerse in if you want to delve into the arguments.

What I see playing out today in the US – and at times in Europe – is the way that, since the end of the Cold War and the supposed triumph of free market ideas in the subsequent 20-plus years, the argument was not made with sufficient force and the benefits not adequately spelled out. So here we are. And one big problem is that what Austrian economist Joseph Schumpeter called the “creative destruction” of capitalism meant that the supposed losers of all this commotion, such as car workers in the UK West Midlands or the US “rust belt” did not get, as far as they could tell, much immediate uplift from the greater overall prosperity that open trade brought. Telling them to “learn to code” just riled them up. (Explaining to an unemployed coal miner or machine tool operator that they should learn a very different skill is difficult, at any age, but particularly if the argument comes from a politician who appears to have never had a real job.) And this, it seems to me, is the fundamental issue: how can a culture of adaptability and can-do attitudes be fostered in a world of constant and at times, disturbing change? (Robert Tracinski makes a good attempt to do so, here.) Because if that does not happen, the populists of the left and the right, whether a Trump, a William Jennings Bryan, etc, will energetically seek to fill the market void. (HL Mencken magnificently destroyed Bryan, who was an opponent of gold-backed money and held many other terrible views that are, I fear, still popular in certain quarters.)

This book, Capitalism In America, from a few years ago by journalist Adrian Wooldridge and former Federal Reserve chairman, jazz musician and economist Alan Greenspan (full disclosure: I have met both of them), gives a good overview of the rise and fall and then rise of arguments about free trade, globalisation, the problems with how the losers from disruption can demand destructive changes, and more. If advocates of free trade like me cannot explain all of this, then the protectionist argument will gain ground, to calamitous effect.

Defining the benefit of spending as who gets the money rather than what gets bought is economic insanity. We might have a little insight there as to why government control of the economy ends up impoverishing.

– Tim Worstall

Those business journalists at Bloomberg ($) have noticed that some investors are betting that Russian debt – a market frozen since the February 2022 invasion of Ukraine – could “thaw out” if there’s a ceasefire/peace deal. But this is a gamble that has potential to go very wrong.

The transactions — revealed here for the first time — are among the clearest indications yet that investors are quietly betting that US President Donald Trump’s overtures to Moscow for a deal to end the war in Ukraine will eventually translate into Russia’s return to the global financial markets. The buyers are wagering that the deeply discounted securities could soar in value if the sanctions imposed on Russia after its invasion of Ukraine in 2022 are lifted.

Money managers, too, say they are receiving approaches from Wall Street sales teams gauging their interest in making bets on the ruble through non-deliverable forwards — derivatives that because they don’t involve a physical Russian asset or individual person aren’t subject to sanctions. The Russian currency has gained 13 percent against the dollar since the start of the year, according to Bank of Russia data.

Goldman Sachs Group Inc. and JPMorgan Chase & Co. are among banks that have been acting as brokers to facilitate growing investor demand for ways to trade Russian-related assets, people familiar with the matter said.

Given the potential for things to go awry, such as if Mr Putin treats a pause in the fighting to re-group and launch another assault, I’d want to be in close touch with any investment managers running my savings plans to be sure that Russian debt, assuming it was ever to be considered in a portfolio, were to take up more than a few percentage points of my total holdings. In fact, I’d want to insist that Russian debt, even after any sort of diplomatic move (regardless of how it is arrived at), is out of bounds.

Competition has utterly transformed telecommunications after the state Post Office monopoly was ended. The same happened with deliveries when Amazon came along with an innovative service. Uber and Airbnb have each transformed their markets.

That is how competition works. It is Schumpeter’s creative destruction. Like evolution, it works by a selective death rate. It is not who owns the production, it is how easy it is for potential competitors to gain access to the market. Growth, productivity and innovation are driven by competition. Producers vie to satisfy the consumers, and those who do so survive, for a time, over those who do not.

One thing that competition ensures is change. It leads to a dynamic economy, just as its absence leads to a static one.

– Madsen Pirie

In all the calls I come across from the Left, it is not often to find examples of how rich people are attacked because if they are allowed to keep more of their wealth (even if is legitimately acquired and without coercion), the money disappears. Forever, kid. It’s lost.

Yes, you read that right. The money vanishes into a black hole. An argument against “trickle-down” economics (which is a term no serious free marketer I have heard of actually uses) is that nothing “trickles” anywhere. Apparently, there is this place, someone on Earth, where money is just sitting around, gathering dust, all on its unproductive exile, just waiting to be rescued by a benevolent State so it can be put back into work. It sounds like a first draft of the plot from the Count of Monte Cristo and the bit about the secret treasure that Edmond Dantes discovered and used to persecute his foes.

Why do I mention this bizarre idea? Because I read it defended and set out in a book, The Future Of Finance: The Rising Tide of Fintech Lending and the Platform Economy, by Francesco Filia and Daniele Guernini, (Whitefox Publishing, 2024). The book is a mostly informative account of how modern digital technology is changing finance. It talks about the role of blockchain; decentralised finance (DEFI) and other developments. It has lots to commend it if you want to understand these ideas, and the use cases in finance for technologies such as AI. But…some of the economic contentions in the book are bonkers.

For example, the authors claim that “we know” that wage growth and equality drive economic growth. (No clear evidicence is given for this contention.) They argue that wage growth continued for about 100 years until 1970, when it apparently stopped.

However, that begs the question of whether there was a lot of equality in that period. Was there a lot of equality, in relative, equality-of-outcome terms, during the “Gilded Age” of the Rockefellers, Carnegies and the rest? (There was not, but the rising tide of wealth nevertheless was considerable.) Was there much of that during the 1920s? I suspect that equality, brought about by steeply progressive tax rates (and they caused issues) did not really manifest itself greatly until after WW2, and even then, given exemptions and other forces, American society in some ways was less egalitarian than in Western Europe.

The authors argue that a labour shortage drove this wealth growth, but surely, absent the restrictive and destructive impact of labour union restrictive practices, it was superior capital investment, and hence superior productivity, that meant tight labour markets coexisted with rising real wages in certain countries. (West Germany rapidly overtook the UK, and it was a country where income tax rates kicked in at higher levels, unions were less obstructive, and there were fewer price controls under the Adenauer administrations than, say, the UK.) The authors make no reference whatsover in this part of the book to investment in capital. But it is total factor productivity (physical capital, human capital, etc) that makes the difference over time to income growth. The US labour market was, relatively, less unionised in the post-war period than the UK one, for example, but the standard of living in the US rose relatively faster, as Milton Friedman pointed out in his book, Free to Choose.

The idea that real incomes have somehow stagnated because wages have stopped rising ignores what might have caused that stagnation. I argue that they get causation back to front. If it is a shortage of labour that causes wages to rise, then surely, absent state intervention, capital will flow into machinery and the like to make up the shortfall, and such a country will also attract immigration (hopefully, of the sort that adds value via skills). In the US, as recounted by Alan Greenspan and Adrian Wooldridge in their masterful account of American capitalism, that’s exactly what happened. During the 19th century, even before the US Civil War, the US saw tremendous growth of labour-saving devices to handle this labour shortage issue. For instance, the McCormick reaper-binder, Singer sewing machine, and more. Light bulbs, early air conditioning…you name it, have also increased returns on human labour because light bulbs allow 24-hour shift work; AC enables places that are otherwise stinking hot to be more economically viable, and so on. And this capital equipment made US workers more productive and increased their real income, other things being equal.

But it is on page 64 that Filia and Guernini ramp up their error wholesale and put forward what I call the “consumption theory of wealth”, which puts spending, rather than investment, innovation and creativity, as the cause of why we are better off: I am going to quote a passage in full:

“When employees and ordinary people (as opposed to odd people, ed?) have more money in their pocket, they spend it. The go out and spend money in restaurants and bars or entertainment venues, they buy new cars or modernise their homes. As a result, that money goes into the real economy to create demand for goods and services and helps businesses prosper and the economy to grow. But when already wealthy people and business owners keep more money via tax cuts, that money is squirrelled away. It’s dumped in offshore trust funds to minimise tax till further or it’s used in stock buybacks. It never reaches the real economy. All it does is to create even greater inequality.” (My emphasis in bold.)

So, if a person saves any money or “squirrels it away”, it is potentially gone. The idea that savings are important, and a source of investment, is totally absent in this account As several on this blog such as Paul Marks regularly point out, a problem in many modern economies is that when investment is financed by central banks’ printing of money, and not real savings made possible by foregoing consumption, it bids up the factors of production, and that without injecting yet more funny money to keep the party going, there’s a crash. The importance of savings cannot be overstated in making sustainable growth possible. The authors claim, with no real evidence, that if money is salted away in a low/no-tax jurisdiction such as the Cayman Islands, Mauritius, Jersey or Dubai, that this money disappears. It’s gone. But that’s plainly rubbish: that money is invested. Why else put it offshore? Even if that money is put into government bonds, that is lent to someone to finance something.

It is true those who use such jurisdictions hope to reduce their overall tax, and in many cases, they defer tax burdens rather that remove them. After all, a person may still want to repatriate their wealth eventually, for whatever reason, and they pay tax on it when that happens. They could, I suppose, give it to charity – but then that money will also go into the “real economy”.

But the idea that money that is not taxed goes out of existence is beyond bizarre. I don’t even know if Thomas Piketty, the French academic who called for progressive taxes and assaults on wealth, went so far into arguing that rich people’s money just vanishes from “real economy”.

Anyway, apart from page 63 and 64, it is a decent book.

UK government tech policy must become libertarian, writes Preston Byrne.

The government wants to boss tech companies around, but it might not get its way any more, because the market is small, tech companies are mobile, and:

…the permanent bureaucracy in the United States which might otherwise have helped the UK apply informal pressure on Americans who dared to disobey its decryption and censorship edicts – none of which, it bears mentioning, are enforceable against an American who refuses them and is happy to avoid setting foot in British territory – is gone.

We should adapt.

If the UK chooses to be the worst place for an AI company, or a social media company, or a digital asset company to incorporate and do business, it will find that it has very few such companies. Regardless of your opinions on how British society should be structured, the NHS, immigration, or the appropriate quantum of social welfare, if you don’t have high tech employers generating revenues and paying taxes, social programs become very difficult to pay for.

Will we get a government capable of making this realisation? Or will we continue to self-destruct?

“Mr. Trump sometimes sounds as if the U.S. shouldn’t import anything at all, that America can be a perfectly closed economy making everything at home. This is called autarky, and it isn’t the world we live in, or one that we should want to live in, as Mr. Trump may soon find out.”

– Wall Street Journal (£)

I think this post is going to annoy Trump defenders, and of course he’s done a few things (shutting DEI down in schools and so on) that I applaud. But this is not the time for whataboutery when considering how terrible Biden was and Harris would have been, as they were and would have been. Those talking points have their place, but now Mr Trump is in office. He’s the President for the next four years.

So there’s no way to finesse this. Tariffs are a form of self-harm, and the reasons given in this particular case shows they are seen as clubs to hit countries with in order to make them change this or that policy. It creates uncertainty, hits inward investment and domestic activity. Domestic and global economic growth will be reduced from where it might have been. Tariffs are taxes, however hard one might try and spin that fact away. Since Adam Smith pointed this all out 250-plus years ago, the damaging impact of tariffs have been widely understood.

Tariffs, particularly given how they been justified and enacted, are a grave mistake by Mr Trump. Trying to claim that the US hit economic heights when tariffs existed in the late 19th century is another case of correlation and causation getting all blurred. The US in the post-Civil War era was a low-tax place: no federal income tax, no Fed, hardly much of a Welfare State as we’d call it, immense inflow of immigrants from places such as Russia, Germany, Italy, Sweden, etc. (Because there was little state welfare, such folk had to work their backsides off, and they did.) Here is an essay that in my view debunks the idea that the post-Civil War tariffs were a good idea.

There are facts that might be a puzzle, but not when you consider that Mr Trump loves tariffs even because they are a weapon. That’s what gets him out of bed in the morning, sometimes for good causes, often not. But the economic rationale is even worse when you consider that American energy costs, thanks to all that fracking he’s in favour of (a plus for him, in my view) means American manufacturing in some ways has a big competitive advantage on Europe, which self-harms because of Net Zero, red tape and high taxation.

Here is an essay I came across via social media and I think it is worth a read:

“I’m going to get a little wonky and write about Donald Trump and negotiations. For those who don’t know, I’m an adjunct professor at Indiana University – Robert H. McKinney School of Law and I teach negotiations. Okay, here goes.

Trump, as most of us know, is the credited author of “The Art of the Deal,” a book that was actually ghost written by a man named Tony Schwartz, who was given access to Trump and wrote based upon his observations. If you’ve read The Art of the Deal, or if you’ve followed Trump lately, you’ll know, even if you didn’t know the label, that he sees all dealmaking as what we call “distributive bargaining.”

Distributive bargaining always has a winner and a loser. It happens when there is a fixed quantity of something and two sides are fighting over how it gets distributed. Think of it as a pie and you’re fighting over who gets how many pieces. In Trump’s world, the bargaining was for a building, or for construction work, or subcontractors. He perceives a successful bargain as one in which there is a winner and a loser, so if he pays less than the seller wants, he wins. The more he saves the more he wins.

The other type of bargaining is called integrative bargaining. In integrative bargaining the two sides don’t have a complete conflict of interest, and it is possible to reach mutually beneficial agreements. Think of it, not a single pie to be divided by two hungry people, but as a baker and a caterer negotiating over how many pies will be baked at what prices, and the nature of their ongoing relationship after this one gig is over.

The problem with Trump is that he sees only distributive bargaining in an international world that requires integrative bargaining. He can raise tariffs, but so can other countries. He can’t demand they not respond. There is no defined end to the negotiation and there is no simple winner and loser. There are always more pies to be baked. Further, negotiations aren’t binary.

China’s choices aren’t (a) buy soybeans from US farmers, or (b) don’t buy soybeans. They can also (c) buy soybeans from Russia, or Argentina, or Brazil, or Canada, etc. That completely strips the distributive bargainer of his power to win or lose, to control the negotiation.

One of the risks of distributive bargaining is bad will. In a one-time distributive bargain, e.g. negotiating with the cabinet maker in your casino about whether you’re going to pay his whole bill or demand a discount, you don’t have to worry about your ongoing credibility or the next deal. If you do that to the cabinet maker, you can bet he won’t agree to do the cabinets in your next casino, and you’re going to have to find another cabinet maker.

There isn’t another Canada.

So when you approach international negotiation, in a world as complex as ours, with integrated economies and multiple buyers and sellers, you simply must approach them through integrative bargaining. If you attempt distributive bargaining, success is impossible. And we see that already.

Trump has raised tariffs on China. China responded, in addition to raising tariffs on US goods, by dropping all its soybean orders from the US and buying them from Russia. The effect is not only to cause tremendous harm to US farmers, but also to increase Russian revenue, making Russia less susceptible to sanctions and boycotts, increasing its economic and political power in the world, and reducing ours. Trump saw steel and aluminum and thought it would be an easy win, BECAUSE HE SAW ONLY STEEL AND ALUMINUM – HE SEES EVERY NEGOTIATION AS DISTRIBUTIVE. China saw it as integrative, and integrated Russia and its soybean purchase orders into a far more complex negotiation ecosystem.

Trump has the same weakness politically. For every winner there must be a loser. And that’s just not how politics works, not over the long run.

For people who study negotiations, this is incredibly basic stuff, negotiations 101, definitions you learn before you even start talking about styles and tactics. And here’s another huge problem for us.

Trump is utterly convinced that his experience in a closely held real estate company has prepared him to run a nation, and therefore he rejects the advice of people who spent entire careers studying the nuances of international negotiations and diplomacy. But the leaders on the other side of the table have not eschewed expertise, they have embraced it. And that means they look at Trump and, given his very limited tool chest and his blindly distributive understanding of negotiation, they know exactly what he is going to do and exactly how to respond to it.

From a professional negotiation point of view, Trump isn’t even bringing checkers to a chess match. He’s bringing a quarter that he insists of flipping for heads or tails, while everybody else is studying the chess board to decide whether its better to open with Najdorf or Grünfeld.”

— David Honig

So there you have it. A bad idea having a damaging impact. Is Mr Trump playing 4-D chess with us all, as his defenders and explainers (including those who consider themselves pro-capitalism seem to be doing in some places that I see on social media), or is this in fact a big error that will eventually hurt America and the freer bits of the world? My worry is that history tells us that, with exceptions, tariff clashes tend to go wrong, lead to slower growth, and even nastier conflicts. It may be that Mr Trump is cleverer than we can appreciate, but I am sceptical.

Not a good start to his time in office. May wiser heads prevail, as they say.

Update: Here is a good article today (4 January) from Daniel Freeman at CapX on how, in his view, Mr Trump has misread the causes of America’s ascent as a business powerhouse.

- Trade makes everyone richer.

- Tariffs make the country applying them poorer.

- The fact that the US government is doing something stupid does not mean you have to join them.

The British economy is lying flat on its back in an alleyway with wee dribbling down its leg.

– Rod Liddle (£)

In the Telegraph’s business section, Matthew Lynn writes about why Santander is thinking of leaving the UK:

Santander’s departure would certainly come as a crushing blow to Rachel Reeves’s ambition to turn the UK into the fastest growing economy in the G7. It emerged during the week that the Spanish bank, a familiar presence in the UK since it acquired Abbey National back in 2004, was considering getting out of the country.

It is not hard to understand why. The returns are pitiful, the regulations are a hassle, costs are rising all the time, and even if profitability does improve, there’s a risk the Government will accuse it of “profiteering” and confiscate whatever money it does manage to make with an extra windfall tax.

For a global bank such as Santander, there are better opportunities elsewhere. It has 76m customers already in South America, for example, and that would seem a better place to deploy its capital, not to mention management time, than the UK.

True, Botin [Santander’s executive chairman] moved quickly to dismiss the reports, telling a panel in Davos how much she loved the UK, and how the bank was committed to the British market for the long term. But then again, she would say that. Nothing will be confirmed until the day a final decision is made.

And yet the simple truth is this. It is a shocking indicator of how poor the prospects are in the UK market that a major corporation such as Santander is even thinking about leaving.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|